[ad_1]

© Getty

Asked last month by a frustrated investor if, “hand on heart”, Royal Dutch Shell was more concerned about “the sustainability of the company or with the sustainability of the planet”, chief executive Ben van Beurden acknowledged that climate change will be “the defining challenge” facing the oil industry for years to come.

He then went on to describe the benefits of energy for millions of people around the world as “quite often a matter of life and death”. He could have been talking about his own industry, which has only just emerged from a brutal downturn and which, according to some, is facing an even graver challenge: whether to invest in oil at a time when climate concerns could see demand peak as early as the 2020s.

It is a question that dominates the energy industry and will determine what the oil majors, including Shell and BP, look like in the future. Driven by investor pressure and a need to rein in costs after the oil price halved in 2014, the industry has largely abandoned new investment in the type of mega-projects, from Arctic exploration to Canadian oil sands, which were once its forte.

————

Investment cut victims

Project Mad Dog 2 (redesigned)

Company BP

Location US, Gulf of Mexico

Love this!

.

.@Regrann from @the_oilfield_zone – Side shot of BP Mad Dog – Submitted by … https://t.co/GBVlCWFxM0 pic.twitter.com/ik6zaazwtf— Rasco FRC Direct (@rascofrcdirect) March 5, 2017

Originally scheduled to start producing oil before 2020, the project was put on ice five years ago as cost forecasts ballooned to more than $20bn. BP has come back with a new plan it believes will cap costs at $9bn, with 140,000 barrels a day of output coming on stream in late 2021.

————

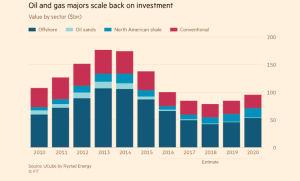

In the second half of this decade total capital expenditure by the large oil and gas groups is projected to fall by almost 50 per cent to $443.5bn from $875.1bn between 2010-15, according to Norwegian consultancy Rystad Energy. Although partly offset by a fall in oilfield development costs, it also coincides with the big groups ploughing more capital into both shorter-term projects that pay off quickly and renewable energy amid fears electric vehicles pose a huge threat to oil’s dominance.

© FT

Click to enlarge

Mr van Beurden told investors by declaring that Shell was no longer an oil and gas group, but an “energy transition company” — a nod to its shift towards a low-carbon energy system.

It is a statement that would have been unthinkable just a few years ago. But persistent cost-cutting and mounting climate concerns have left many in the sector worried that the industry is making a miscalculation. They fear it is turning its back on many big oil and gas projects before efficiency gains, renewables, electric cars and efforts to conserve fossil fuels are able to cap consumption. The result could be supply shortfalls and price rises, storing up a problem for the global economy.

“It’s not wise to be cavalier about a lack of investment,” says Stewart Glickman, an energy equity analyst at CFRA. “The drop over the past four years eventually will have an impact on crude prices.”

He adds that while investment in US shale has grown as companies look to short-cycle projects, bottlenecks and the declining quality of reserves mean it alone might not be able to fill the gap. “To blithely assume that because [the US shale industry] has been able to generate enough production so far that we’ll be able to continue doing so is a risky expectation,” he says.

Estimates for when oil demand will peak vary wildly. Some experts say it could happen as soon as 2023, others put it off to 2070. That lack of consensus presents a danger, critics say, that the oil groups are being pushed — against their instincts — into shelving complex long-term investments just as demand for oil nears 100m barrels a day for the first time as emerging economies in Asia and Africa expand.

“There is so much uncertainty,” says Andrew Gould, former chairman and chief executive of oilfield services company Schlumberger. “It’s increasingly difficult now to get boards to sign off on projects that have a 20-25 year life.”

Cost deflation has allowed approval of certain projects such as Mad Dog 2, BP’s deepwater offshore project in the US, while others are on hold or have been scaled back. Such projects would have provided a baseline cushion of supplies to smooth out any future market shortages or additional demand. If that supply is not there, some fear a backlash from consumer countries as oil prices escalate.

Officials in India, which will lead oil demand growth in the coming years, are already anxious after the price hit $80 a barrel earlier this year, while eurozone governments will come under pressure should pump prices rise.

For big energy companies and resource-rich economies reliant on vast oilfields for public spending, the fear of demand hitting a peak is pronounced. That it is being discussed at a time when demand has actually been growing at an average of 1.7m barrels a day every year since 2014 — double the rate at the start of this decade, when oil averaged close to $100 a barrel — is mystifying to some.

———-

Investment cut victims

Project Bonga Southwest (delayed)

Company Shell

Location Nigeria

Fears over renewed militancy after Bonga #oil field shut-down | TheCable https://t.co/vQQUp2L39T #TheCablePetrobarometer pic.twitter.com/MgXSyIWasB

— TheCable (@thecableng) February 5, 2018

Shell’s plan to develop its Bonga oilfield in deep water off Nigeria has been delayed several times since 2015. Having started pumping crude in 2005, Bonga’s $12bn extension was expected to add up to 175,000 barrels a day to output but its future now depends on cutting costs.

———-

Tony Hayward, the former chief executive of BP who is now chairman of the mining and trading group Glencore, casts doubt on the whole strategy, hinting that placating shareholders was winning out against their better interests.

“I don’t think the supermajors really believe the long-term story of peak demand,” Mr Hayward told the Financial Times last week. “Looking at the trajectory, we’re more likely to have a supply crunch in the early 2020s.”

Investors are driving this shift. Mainstream asset managers and pension funds are increasingly concerned about the potential financial impact of global warming and of policies to limit it.

Legal & General Investment Management, one of the biggest owners of BP and Shell shares through the UK pension funds it manages, has led the way in telling them to focus less on the risks of short-term price moves, and prepare instead to manage an industry in decline.

Nick Stansbury, who heads L&G’s strategy in energy and commodity markets, says their argument is that while it is impossible to predict exactly when oil demand will peak, they are now convinced the moment is coming. Electric vehicles, a backlash against plastics and the rise of alternative fuels all threaten to cap oil demand, L&G argues.

Oil groups should therefore, he says, avoid projects that take 10 or more years to become profitable — which used to be the industry standard. Instead they should focus on maximising returns to shareholders, including eventually returning capital rather than trying to transform themselves into renewable companies in which they lack expertise.

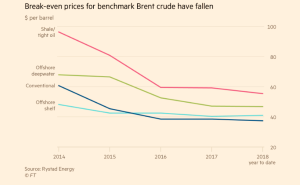

© FT

Click to enlarge

“We’re not in the school of thought that says peak oil comes in 2021 or that there’s no need to invest in any new oil projects at all,” Mr Stansbury says. “But what we do want them to commit to doing . . . is become the cash flow engines that fund the energy transition.”

He says such a strategy poses risks for the wider world in the form of volatile oil prices, but argues that funds investing other people’s money in energy companies have to remain focused on any longer-term risks.

It is part of a bigger debate. Investors often deemed the oil majors’ spending programmes were far too wasteful when oil was above $100 a barrel, yielding inadequate returns. The 2014 oil price crash forced an overhaul in their approach to investment.

© Getty

Presiding over an era of transition: Shell chief executive Ben van Beurden

Brian Gilvary, BP’s chief financial officer, insists it is not just investor fear of peak demand that has seen the company move away from longer-term oil and gas projects. In the wake of the 2014 price drop— triggered in part by the rise of US shale and subsequent supply glut — he argues it is sensible for companies such as BP to focus on the fastest and cheapest projects.

“We’re becoming more efficient at how we deploy capital,” Mr Gilvary says. He adds that BP and other energy groups are ploughing a middle road: raising oil production by using technology to sweat more barrels out of existing fields, while also funnelling smaller amounts of capital into so-called short-cycle projects such as US shale.

“We are not seeing any indication that there is [a supply crunch] coming, but we understand the fear,” says the BP executive. “We are continuing to grow our business . . . and we still see sufficient activity.”

———-

Investment cut victims

Project Rosebank (delayed)

Company Chevron

Location UK, North Sea

© Getty

Just off the west coast of Shetland. the Rosebank field was discovered in 2004. Chevron was examining the feasibility of developing a reported $10bn project shortly before the oil price crash.

In 2016 it cancelled a $1.8bn order for a floating production and offloading (FPSO) vessel to service the field. Chevron has said the project remains under consideration and it is working on its design and economics.

———-

Chris Midgley, a former chief economist at Shell who is now the head of analytics at S&P Global Platts, believes BP’s approach makes sense but warns that the biggest risk will come in five to seven years when focusing investment largely on existing fields could fail to yield enough baseline production. Even if that led to higher prices, oil companies may not respond.

“If we do get higher prices, unlike previous cycles the [international oil companies] might choose to effectively sit on their hands, saying they’ll use the windfall to accelerate into the energy transition rather than making more [oil] investments,” he says. Any prolonged period of higher prices that might follow would inevitably lead to a curb in consumption. “That would be . . . recessionary for the entire economy,” he says.

For now the strategy appears to be working. According to Wood Mackenzie, an oil consultancy, output growth among the oil majors is expected to rise, on average, by approximately 3.5 per cent a year between 2017 and 2020.

After a more than 40 per cent drop in conventional onshore drilling globally from 2014-16, it has since risen by 17 per cent, says Rystad Energy. In US shale oilfields, drilling dropped by 55 per cent over the same period but has increased by 65 per cent since 2016, illustrating the popularity of short-cycle projects. ExxonMobil, which has been slower to address climate risk than its peers, has said there would still be a need for trillions of dollars of investment in new oil and gas production, even in a world where temperature rises would be limited to 2C.

Meanwhile, the recovery in oil prices has largely been driven by factors outside the energy companies’ control. Demand is strong, Opec and Russia purposely trimmed back production in 2017, and since then output in Venezuela has fallen because of the economic and political crisis gripping the country.

US president Donald Trump’s decision to withdraw from the Iran nuclear deal and reimpose sanctions on the country’s energy exports was the final bump to take oil above $80 per barrel. But since then prices have fallen back to around $74 as Saudi Arabia and Russia discuss releasing additional barrels on to the market — something oil ministers will debate at Opec this week.

© FT

Click to enlarge

Some of the biggest oil traders, however, remain unconvinced that it is possible to keep the market well supplied with short-term investments.

Pierre Andurand, a hedge fund manager who oversees more than $1bn in investor money and bets on oil price moves, says it could hit $150 a barrel within two years, partly due to the focus on peak demand while consumption is still rising. Other industry executives and analysts see a lower rise but believe prices will return to above $100 a barrel.

“There is pressure from investors for these companies not to invest too much in oil, but at the same time we don’t see electric cars having a major impact on demand growth for at least another decade,” he says. “It is not obvious to me where this supply growth is going to come from.”

Some dismiss this as scaremongering, saying the industry has shifted from an age of perceived scarcity to abundance, meaning much of this long-term investment into big projects is unnecessary.

For now Mr van Beurden is betting that Shell has made the right calculations. A slightly higher oil price would not be the worst thing in the world for his company as it grapples with the energy transition. After all, no chief executive wants to be left holding multibillion-dollar oilfields the world no longer wants or needs.

Follow us on Facebook, and on Twitter

[ad_2]